, you have now set your site language to English. If you'd like to change your language preference again, simply click on one of the other flags.

, you have now set your site language to English. If you'd like to change your language preference again, simply click on one of the other flags. を選択して頂くと、言語設定が日本語に切り替わります。設定変更後は以下の機能が利用可能です。

を選択して頂くと、言語設定が日本語に切り替わります。設定変更後は以下の機能が利用可能です。

,可将网站语言设置为中文。这能帮助您:

,可将网站语言设置为中文。这能帮助您:2020 Vision

The reduction of the IMO global fuel sulphur cap to 0.5% will come into force on 1 January 2020. Shipowners have some very difficult and important decisions to make on how to comply with these stringent requirements.

The requirement to reduce the maximum sulphur content of fuel down to 0.5% from its current limit of 3.5% in 2020 is not a surprise to the industry. It was added to MARPOL Annex VI back in 2008 but at that time an option existed to defer this change to 2025.

However, in 2016 IMO rejected this option to defer. 2020 was set in stone and it has been made clear that there will be no postponement, grace period or transition period.

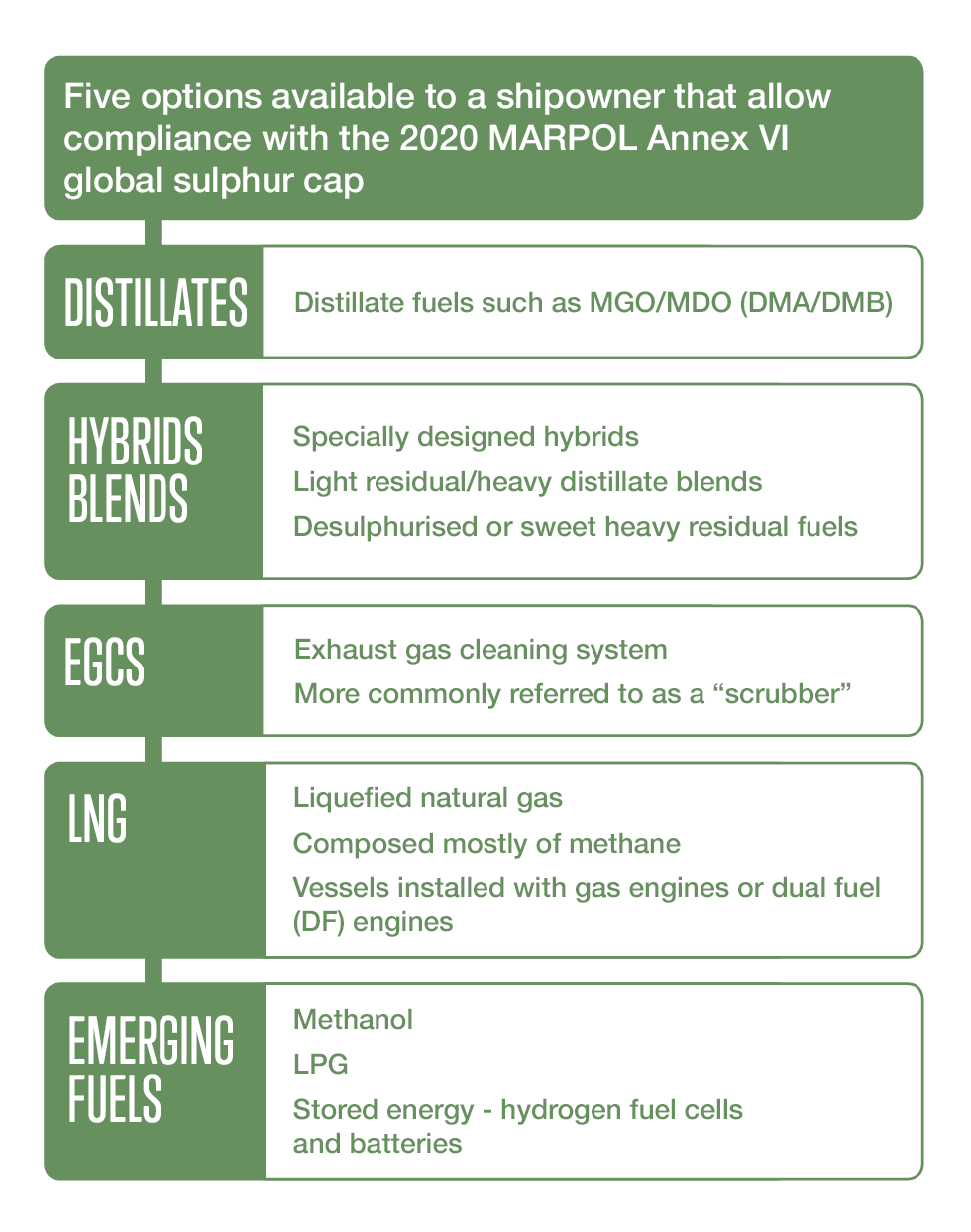

Speaking broadly, there are five options available to a shipowner that allow compliance with the 2020 MARPOL Annex VI global sulphur cap (see below):

It has already become apparent that the majority of shipping companies intend to burn distillate fuels in their vessels’ engines and boilers. In time, it is likely that a proportion will turn to hybrids, blends or any newly developed compliant residual fuels, depending on bunker prices and availability. A smaller proportion has opted to install scrubbers and continue burning high sulphur residual fuels.

Some shipowners are opting for LNG but retaining the ability to burn distillates by installing dual fuel (DF) engines. We expect the emerging fuels market will be very niche.

There are pros and cons with each, mostly concerning fuel availability, onboard fuel management, capital expenditure and operational expenditure and maintenance requirements. It is not a simple choice and the decision on what method of compliance is best depends on a number of factors, such as vessel type, trading area and indeed its expected remaining life.

The proportion of time spent within emission control areas (ECAs) should also be considered as well as the impact of changing over fuels when entering or leaving these areas. The 0.1% sulphur cap currently in operation within the ECAs will remain in force and it is possible that new ECAs may emerge in coming years.

The challenges are not all just technical. Charterparties, where the obligation to provide bunkers is on the charterer will require close attention.

This is a far more pressing matter for vessels already in long-term charterparties that span the enforcement date of 1 January 2020.

In the next issue of Signals, we will take an in-depth look at the 2020 global sulphur cap, focusing on what it means for shipowners and the impact on charterparties. In the meantime, if you have any charterparty related questions please contact our FD&D team.

Find out more

Visit our 2020 Insights area.

Author: Alvin Forster